Annuities are financial products that offer a guaranteed income stream and are usually purchased by retirees to provide a steady cash flow during their retirement years. They are designed to address the risk of outliving one's savings or assets. Individuals who invest in annuities cannot outlive their income stream, as the annuity contract guarantees regular payments for a fixed period or for the rest of their lives. The two basic types of annuity contracts are immediate and deferred, with various options available such as life-only, period certain only, certain and life, and installment refund. The specific type of annuity an annuitant chooses will determine whether payments continue or stop after their death.

Explore related products

What You'll Learn

![]()

Annuities are a contract between a purchaser and an insurance company

An annuity is a contract between a purchaser and an insurance company. The purchaser agrees to make a lump-sum payment or a series of payments in return for regular disbursements, beginning either immediately (within 12 months) or at some future date. The goal of most annuities is to provide a steady stream of income during retirement for a specified period or for the remainder of one or more lives. This means that an annuitant cannot outlive the income payments.

Annuities are often used to address the risk of outliving one's savings or financial resources. They are designed to provide a steady cash flow for people during their retirement years, guaranteeing retirement income. The invested cash is illiquid and subject to withdrawal penalties, so it is generally not recommended for younger individuals or those with liquidity needs. Annuities can be complex, and the associated fees can be high, so it is important to consult a professional before purchasing an annuity contract.

There are two basic kinds of annuity contracts: immediate and deferred. Immediate annuities are purchased with a single premium, and periodic payments are generally equal and made monthly, quarterly, semi-annually, or annually. Deferred annuities, on the other hand, do not immediately begin making payments but wait for a specific time to start. The buyer usually contributes over a years, and the contributions grow through interest credited and compounding interest.

Annuity contracts can encompass up to four entities: the issuer (usually an insurance company), the owner of the annuity, the annuitant, and the beneficiary. The owner is typically the purchaser and the person who receives the periodic payments. The annuitant is the individual whose life expectancy is used to determine the payout amount and when the payments will start and cease. The beneficiary is the individual who will receive a death benefit when the annuitant dies.

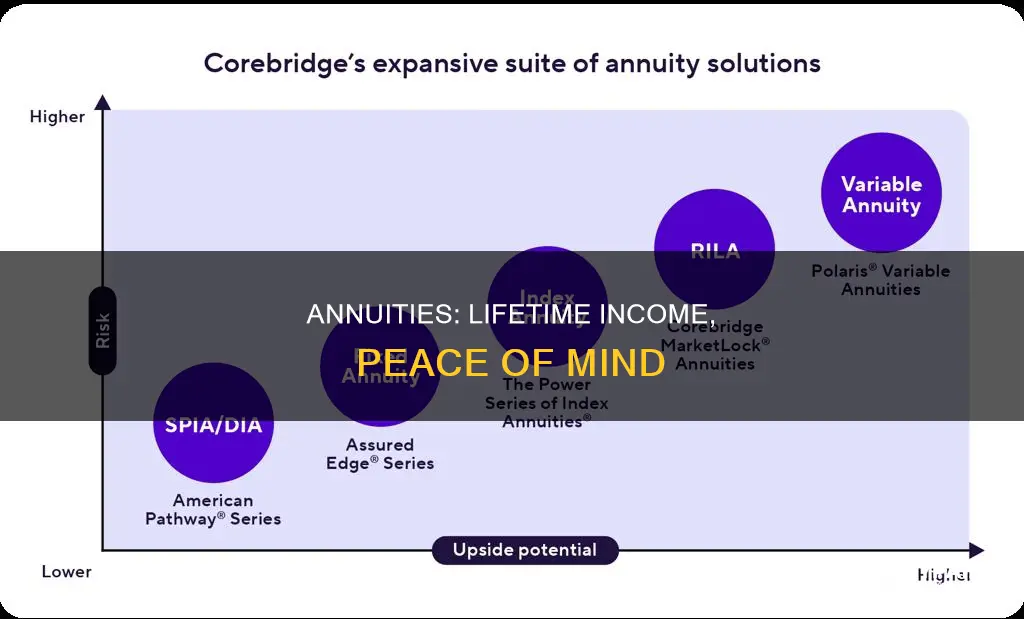

Annuities can be structured in different ways, including fixed, variable, or indexed to an equity index. They may also offer different payout and beneficiary options, such as life-only, period certain only, certain and life, and installment refund. It is important to understand the specific details and obligations outlined in the annuity contract before purchasing.

Easy Fender Repair: Scrapes and Paint Fixes

You may want to see also

Explore related products

![]()

Annuities are used primarily for retirement income

An annuity is a contract issued and distributed by an insurance company and bought by individuals. The insurance company pays out a fixed or variable income stream to the purchaser, beginning right away or at some future date, in exchange for premiums paid. Annuities are financial products that offer a guaranteed income stream and are usually bought by retirees. They are used primarily for retirement income purposes.

Annuities are designed to be a long-term part of a financial plan, along with other retirement income streams. They can help individuals address the risk of outliving their savings. The money invested in an annuity is illiquid and subject to withdrawal penalties, so it is generally not recommended for younger individuals or those with liquidity needs. Annuities can be purchased with either pre-tax or after-tax dollars.

Annuities can be immediate or deferred. Immediate annuities are often purchased by individuals of any age who have received a large lump sum of money and prefer to exchange that money for future cash flows. Deferred annuities, on the other hand, are structured to grow on a tax-deferred basis and provide annuitants with guaranteed income that begins on a specified date.

Annuities can also be fixed, variable, or indexed. Fixed annuities provide a guaranteed income stream, with the insurance company bearing the investment risk. Variable annuities offer the potential for higher returns but also come with higher risks. Indexed annuities provide returns based on the performance of a specific index, such as the S&P 500.

Annuities are a popular way to turn part of an individual's retirement savings into a stream of steady income to live on during retirement. They are appropriate for investors who want stable and guaranteed retirement income. Annuity holders can't outlive their income stream, which hedges longevity risk.

Cropping Images in MS Paint: Keep Only the Selection

You may want to see also

Explore related products

![]()

Annuities can be immediate or deferred

Annuities are financial products that offer a guaranteed income stream and are usually bought by retirees. They are used primarily for retirement income purposes. Annuities can be immediate or deferred.

An immediate annuity is an annuity contract in which payments start within 12 months of the date of purchase. The immediate annuity is purchased with a single premium and periodic payments are generally equal and made monthly, quarterly, semi-annually or annually. The payout amount for immediate annuities depends on market conditions and interest rates.

A deferred annuity, on the other hand, is a contract with an insurance company that promises to pay the owner a regular income or a lump sum at some future date. Deferred annuities are considered long-term investments. They have two phases: the accumulation phase and the payout phase, which is deferred for at least one year after purchasing the annuity. During the accumulation phase, one or more premium payments are made, and the funds receive interest or are invested, growing tax-deferred.

The choice between a deferred and immediate annuity payout depends largely on one's savings and future earnings goals. Immediate payouts can be beneficial if you are already retired and need a source of income to cover day-to-day expenses. Deferred payouts may be ideal if you do not require supplemental income yet, as the underlying annuity can build more potential earnings over time.

Annuities can help address the risk of outliving one's savings. Individuals who invest in annuities cannot outlive their income stream and this hedges longevity risk.

Spray-Painting Your Rims: Keep the Tires On!

You may want to see also

Explore related products

![]()

Annuities can be fixed, variable or indexed

Annuities are financial products that offer a guaranteed income stream, usually for retirees. They are designed to address the risk of outliving one's savings. Annuities can be structured in various ways, offering investors flexibility.

Annuities can be fixed, variable, or indexed. Fixed annuities offer a guaranteed, predetermined interest rate for a specified period, providing predictable growth regardless of market conditions. They are considered lower-risk investments, offering stable and predictable returns. Fixed annuities are ideal for those with conservative risk tolerance.

Variable annuities, on the other hand, offer variable returns instead of fixed returns. With these, investors can decide how much risk they want to take on for their investments. Variable annuity contracts typically offer professionally managed portfolios called subaccounts, which function like mutual funds. Variable annuities allow investors to benefit from potential positive returns but also carry the risk of market downturns.

Indexed annuities, also known as fixed-indexed annuities (FIAs), tie interest earnings to the performance of a market index, such as the S&P 500 or the Nasdaq 100. When the index value increases, the annuitant is credited with interest. However, if the index has negative performance, no interest is earned for that year. Indexed annuities protect the principal from any downside loss in value, ensuring it is never less than zero.

Annuities are complex financial vehicles, and it is recommended to consult a financial professional to determine which type of annuity is suitable for one's needs.

Paint Protection Film: Windshield Wonder or Waste?

You may want to see also

Explore related products

![]()

Annuities can be qualified or non-qualified

Annuities are financial products that offer a guaranteed income stream and are typically purchased by retirees. They are used to address the risk of outliving one's savings. Annuities can be qualified or non-qualified, and this distinction is important as it determines the tax status of the annuity.

A qualified annuity is funded with pre-tax dollars, which gives an immediate tax benefit to the investor. Contributions to a qualified annuity reduce taxable income in the year of contribution. Taxes are then deferred until withdrawals are made, and these withdrawals are taxed as ordinary income. Qualified annuities are often set up by employers as part of a company-sponsored retirement plan, and they can be beneficial for tax-deferral and guarantees. Examples of qualified plans include 401(k) plans and 403(b) plans.

On the other hand, a non-qualified annuity is funded with after-tax dollars. There is no immediate tax benefit to contributing to a non-qualified annuity, but taxes are only paid on the earnings at the time of withdrawal, not the principal. Non-qualified annuities offer tax-deferred growth and potential tax benefits during withdrawals. However, they do not have RMDs (required minimum distributions), which means the annuitant has more control over when they access their funds.

It is important to note that the tax treatment of withdrawals can vary and can be complex, so it is recommended to consult a tax expert to navigate the differences between qualified and non-qualified annuities. Additionally, annuities can be structured as either fixed or variable instruments, providing regular periodic payments or larger future payments based on the performance of the annuity fund, respectively.

In summary, the key difference between qualified and non-qualified annuities lies in the tax treatment of contributions and withdrawals. Qualified annuities offer immediate tax savings, while non-qualified annuities may provide potential tax benefits during withdrawals. The choice between the two depends on an individual's specific retirement needs and tax situation.

Shooting People with Paintballs: Is it Legal?

You may want to see also

Frequently asked questions

An annuity is a contract between a purchaser and an insurance company in which the purchaser agrees to make a lump-sum payment or series of payments in return for regular disbursements, beginning either immediately (within 12 months) or at some future date.

Individuals who invest in annuities cannot outlive their income stream. Annuities are designed to provide a steady cash flow for people during their retirement years to alleviate the fear of outliving their assets. Annuities deal with longevity risk, or the risk of outliving one's assets.

The two basic kinds of annuity contracts are immediate and deferred. An immediate annuity is an annuity contract in which payments start within 12 months of the date of purchase. A deferred annuity, on the other hand, does not immediately begin making payments but instead waits for a specific time to start. Other types of annuities include fixed, variable, or indexed annuities.

When you die, your annuity will either end, continue for a specified period for your beneficiary, or continue making payments to the surviving person (if it is a joint annuity), depending on the options you chose when you purchased it.