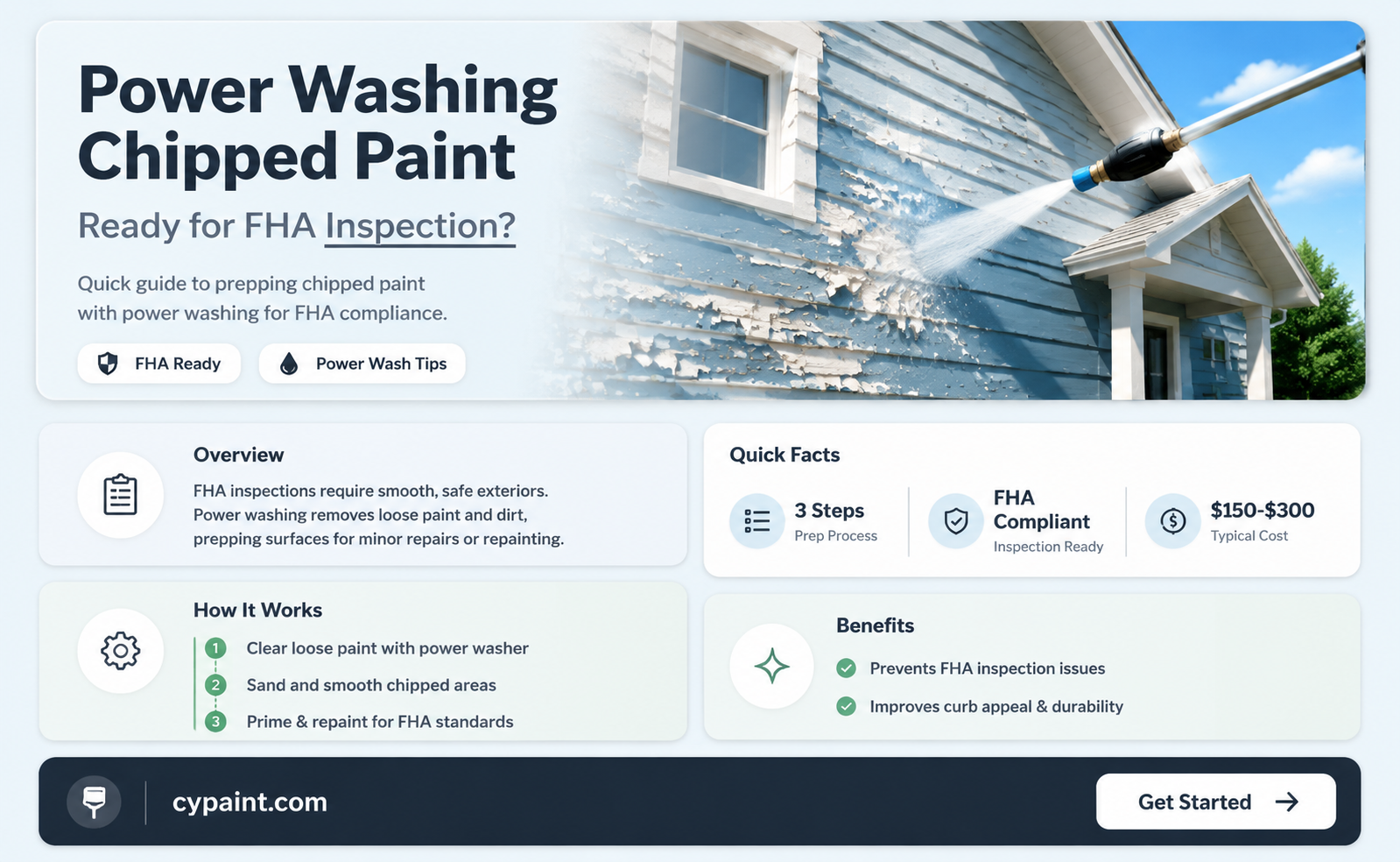

FHA appraisers are required to note the condition of painted surfaces and call for the removal of any peeling or chipping paint. This is because, for homes built before 1978, there is a risk of lead-based paint, which poses a serious health concern. FHA guidelines require the seller to provide full disclosure of any known lead hazards. If a home was built after 1978, the appraiser must report all defective paint surfaces on the exterior and require repairs if the subsurface is exposed to the elements. Repairs for chipping paint can sometimes be waived, but this is not always the case.

| Characteristics | Values |

|---|---|

| FHA inspection requirement for chipped paint | If the property was built before 1978, the seller must disclose any information about lead-based paint and hazards. FHA requires repairs for defective paint surfaces for houses built before 1978. |

| FHA inspection requirement for chipped paint | If the property was built in 1978 or later, repair is only required when missing paint exposes the subsurface to the elements. |

| Peeling paint removal process | Scrape off the old paint, apply a new coat of paint, and remove the paint chips. |

| Waiving the 10-day window for lead-based paint inspection | Buyers can waive the 10-day window for lead-based paint inspection but cannot waive the repairs required by the appraiser. |

Explore related products

What You'll Learn

![]()

FHA loans and pre-1978 homes

FHA loans are a good option for homebuyers who have not saved much for their down payments, as they can be as low as 3.5% of the purchase price. FHA loans are also available for a variety of home needs, including building a house from the ground up with an FHA One-Time Close construction loan.

If you are planning on selling or buying a home built before 1978 with an FHA loan, you need to be aware of the possibility of lead-based paint. FHA home loan rules require the seller to provide full disclosure of any known lead hazards. The seller must disclose any information known about lead-based paint and lead-based paint hazards before selling the house, in accordance with the HUD-EPA Lead Disclosure Rule. The buyer must be fully informed as to the nature of the lead hazard if known. In such cases, there are additional requirements such as providing the borrower with an opportunity to conduct a lead paint inspection/risk assessment. The borrower must be given ten days to accomplish the assessment or inspection.

If a home was built prior to 1978, lead contamination could be an issue. Checking for the possibility of peeling or chipping paint is a must for any appraiser completing an appraisal for FHA financing. Peeling, chipping, or flaking paint must be removed by the approved method of scraping the defective surfaces and then reapplying new paint. The FHA appraiser must "note the condition and location of all defective paint and require repair in compliance with 24 CFR § 200.810(c) and any applicable EPA requirements."

You can waive your right to a 10-day window to perform a lead-based paint safety inspection for an FHA loan. However, you cannot waive peeling or chipping paint repairs required by the appraiser. You can resolve hazardous or cosmetic issues after closing with the FHA 203k program.

Clark+Kensington: Satin Enamel Paint for Interiors?

You may want to see also

Explore related products

![]()

Lead-based paint hazards

Lead-based paint is a highly toxic metal that can cause a range of health problems, especially in young children. Lead-based paint was banned for residential use in 1978, but homes built before 1978 are likely to have some lead-based paint. If the paint is in good shape, it is usually not a problem. However, if the paint is deteriorating (peeling, chipping, chalking, cracking, damaged, or damp), it is a hazard and needs immediate attention.

Lead-based paint may also be a hazard when found on surfaces that children can access, such as stairs, railings, banisters, and porches. If a home was built prior to 1978, lead contamination could be an issue. FHA home loan rules require the seller to disclose any known lead hazards. In such cases, the borrower must be given the opportunity to conduct a lead paint inspection or risk assessment.

To address lead-based paint hazards, it is important to remove any flaking or peeling paint down to the bare surface and repaint. It is crucial to pay close attention to paint flakes that may fall during the removal process as they still present health and safety concerns. Any loose paint chips should be picked up carefully with a paper towel and discarded, and the surface should be wiped clean with a wet paper towel. It is also important to keep children away from housing undergoing renovation and from participating in activities that disturb old paint.

A risk assessment can help determine if there are any serious lead hazards and what actions need to be taken to address them. This includes testing paint and dust from the home for lead and having the soil tested as well. It is recommended to consult with a certified lead professional before beginning any renovation, repair, or painting projects that could create toxic lead dust.

Safe Paint Disposal in Dauphin County, PA

You may want to see also

Explore related products

![]()

FHA appraisal requirements

FHA loans are a great option for first-time homebuyers. If you're planning to get a mortgage backed by the Federal Housing Administration (FHA), the house you want to buy requires an appraisal that meets FHA standards. A home appraisal is an estimate of the market value of a property. Since a third party performs the appraisal, the market value is not influenced by the buyer or the seller. FHA appraisal guidelines tend to be more stringent than conventional appraisal rules, and they're designed to ensure the home is "safe, sound and secure".

FHA appraisers adhere to HUD guidelines for minimum property standards. The following are some of the appraisal requirements or repair items that may be necessary for a property to be approved for an FHA loan. Please note that this list is not exhaustive, and certain requirements, such as security bars on windows, may vary depending on the specific property:

- The property must have an undamaged exterior, foundation and roof.

- All relevant utilities, including gas, electricity, water and sewage, must be functioning properly.

- The property must have a working, permanent heating system that can heat the property adequately.

- All surfaces must be free of chipping or peeling lead-based paint.

- There must be adequate access to attic spaces and natural ventilation in crawl spaces.

- The property must not have interior and exterior health and safety hazards, such as no handrails on steep staircases.

If the property doesn't meet the criteria, the appraiser will suggest repairs that improve the property to FHA standards. Both the buyer and the lender receive a copy of the FHA appraisal, which is valid for 180 days. It's up to the lender to approve, conditionally approve or reject the property.

Painted Mason Jars: Curing in the Oven

You may want to see also

Explore related products

![]()

FHA loan approval conditions

The Federal Housing Administration (FHA), which is part of the US Department of Housing and Urban Development (HUD), provides mortgage insurance on loans made by FHA-approved lenders. FHA loans are designed to make the path to homeownership easier, with low down payment requirements, low closing costs, and easy credit qualification.

Credit Score

A minimum credit score of 580 is required to qualify for an FHA loan. A score between 500 and 579 will require a larger down payment of 10%. Additionally, for an FHA Streamline refinance, Rocket Mortgage requires a minimum score of 580, while a cash-out refinance requires a median score of 620.

Down Payment

The down payment can be as low as 3.5% of the purchase price. The down payment is calculated as a percentage of the purchase price, determined by the loan requirements. The FHA lender must verify the source of the down payment funds, which can include cash, cashed-in investments, gift funds, or other approved means.

Mortgage Insurance

Mortgage Insurance Premium (MIP) is required for FHA loans. Depending on the loan terms and conditions, MIP may be required for 11 years or the lifetime of the mortgage.

Debt-to-Income Ratio

The borrower's debt-to-income ratio must be less than 43%. This ratio is used to calculate whether the borrower can financially manage the demands of owning a home.

Primary Residence

The property must be the borrower's primary residence, and they must occupy it within 60 days of closing.

Steady Income and Employment History

The borrower must have a steady income and proof of employment. They must provide pay stubs, W-2s, federal tax returns, and bank statements to demonstrate their employment history.

FHA Inspection and Appraisal

An FHA inspection is required to ensure the property meets minimum standards. The home must also be appraised by an FHA-approved appraiser.

Peeling Paint

If the home was built before 1978, peeling or chipping paint must be addressed according to FHA and EPA requirements as a condition of loan approval. This is due to the potential for lead-based paint, which can cause serious health issues. The seller must disclose any known lead-based paint hazards. Repairs must be made by scraping and repainting the affected surfaces.

Timeframe

The borrower must be given a timeframe, typically ten days, to accomplish the inspection or assessment.

FHA 203(k) Loan

The FHA 203(k) loan is a minimum of $5,000 and is designed for home repairs and improvements, with a completion timeframe of 6 months. There are two types: Standard loans, which offer more flexibility, and Limited loans, which require less paperwork.

It is important to note that specific requirements may vary depending on the lender, and it is always advisable to consult professionals before making any decisions regarding FHA loans.

Mastering the Art of Painting a Tall, Skinny Giraffe

You may want to see also

Explore related products

![]()

FHA repair programs

FHA loans are insured by the government to increase the availability of affordable housing in the US. These loans are backed by the FHA, which protects lenders from significant losses. FHA repair programs are available to help finance home repairs or improvements.

The FHA 203(k) rehabilitation mortgage insurance program lets homebuyers and owners finance up to $35,000 into their mortgage for home repairs or improvements. The Home Equity Conversion Mortgage (HECM) program is a type of home loan known as a reverse mortgage, insured by the government. The HECM program lets you withdraw some of your home's equity to use for home maintenance, repairs, or living expenses.

The FHA Repair Escrow program can be used to finance the purchase of a home that needs minimal repairs. This program provides mortgage insurance for borrowers to purchase a HUD home as a principal residence. The FHA Repair Escrow loan option allows borrowers to finance up to $10,000 in home repairs.

FHA loans can be used to repair or remodel homes. You might need to do a relatively minor repair or a major alteration. The FHA has a maximum loan amount that it will insure, known as the FHA lending limit.

If a home was built before 1978, lead-based paint may be an issue. FHA home loan rules require the seller to provide full disclosure of any known lead hazard. If there is peeling or chipping paint, it must be removed by scraping the defective surfaces and then reapplying new paint.

In conclusion, FHA repair programs can help finance home repairs and improvements, including those related to lead-based paint hazards in homes built before 1978. These programs can enable borrowers to purchase homes that need minimal repairs and provide assistance for both first-time and existing homeowners.

Preserve Your Silk Paints Art: Tips and Tricks

You may want to see also

Frequently asked questions

Yes, chipped paint can be a dealbreaker for FHA loans, especially if the property was built before 1978, as there could be lead-based paint, which poses a health risk.

The procedure for dealing with chipped paint involves scraping the defective surface, removing any paint chips, and then applying a new coat of paint.

Yes, you can waive the 10-day window for a lead-based paint inspection, but you cannot waive the repairs required by the appraiser.