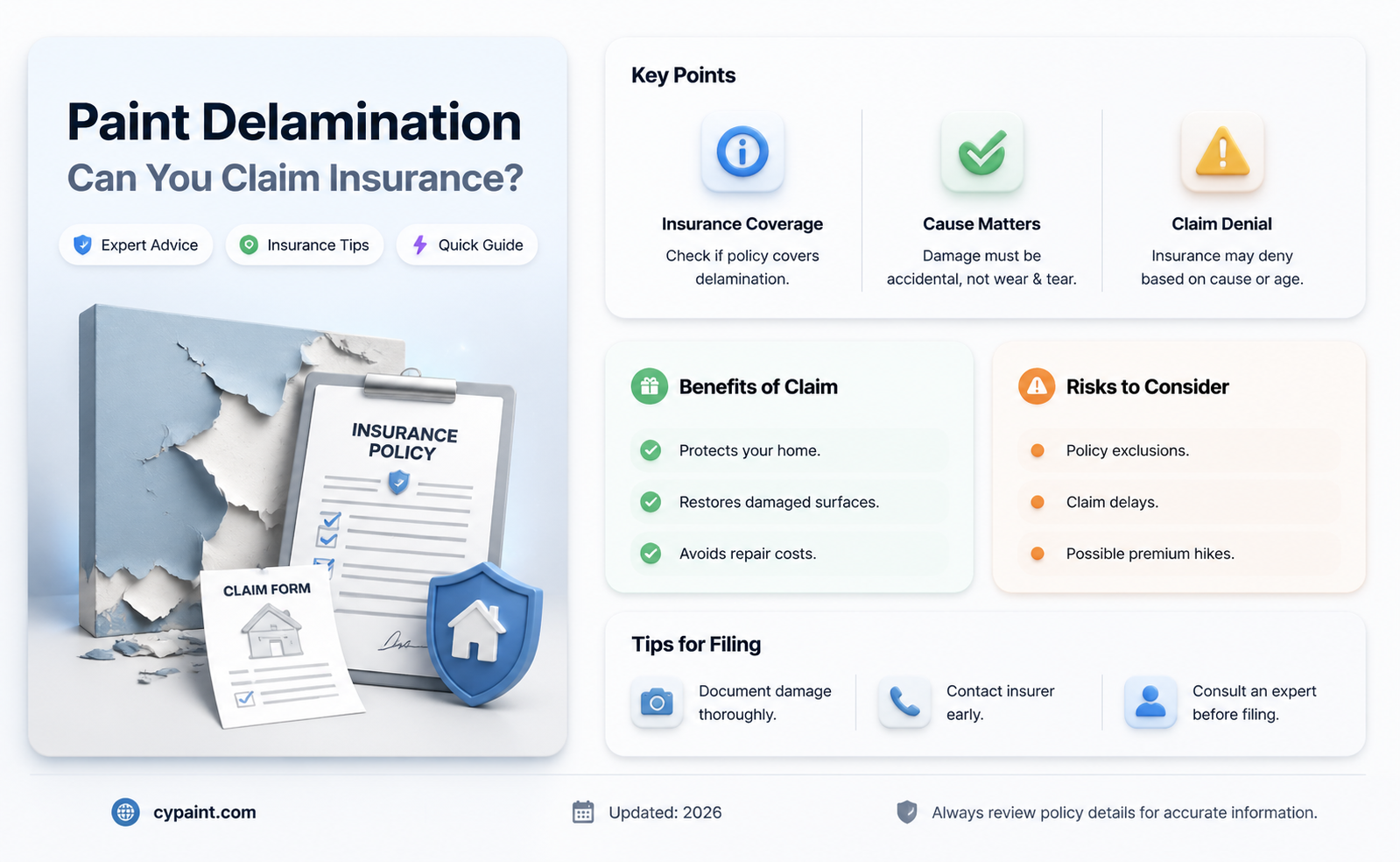

Whether you're dealing with paint damage to your home or vehicle, understanding your insurance coverage is crucial before filing a claim. Paint damage can be covered by insurance in certain circumstances, such as collisions or comprehensive coverage for vehicles, and unforeseen events like fires, vandalism, or natural disasters for homes. However, it's important to carefully review your policy, as exclusions and limitations may apply. Understanding the cause of the damage is essential, as normal wear and tear or neglect may not be covered. Proper documentation, including photographs, videos, and written accounts, is also necessary to support your claim. While insurance can provide financial protection, it's important to consider the cost-effectiveness of filing a claim for minor paint issues.

| Characteristics | Values |

|---|---|

| Car insurance coverage for paint damage | Covered under Collision or Comprehensive coverage |

| Collision coverage | Pays for damage if the car hits another vehicle or object, or is hit by another vehicle |

| Comprehensive coverage | Pays for damages not related to a collision, including vandalism and natural disasters |

| Deductible | The policyholder's share of the cost for a claim, to be paid before insurance coverage begins |

| Minor cosmetic damage | May not meet the deductible, making a claim unnecessary |

| Vandalism | Covered under comprehensive coverage |

| Natural disasters | Covered under comprehensive coverage |

| Exclusions | Negligence or failure to maintain the painted area properly |

| Home insurance coverage for paint damage | Typically covers damages caused by unforeseen events such as fires, vandalism, or natural disasters |

| Home improvement projects | May be included in some policies |

| Limitations | Normal wear and tear or neglect may not be covered |

| Documentation | Photographic or video evidence, original receipts, contracts, appraisals, and a written account of the incident |

Explore related products

What You'll Learn

![]()

Collision and comprehensive coverage

When deciding whether to add collision and comprehensive coverage to your policy, consider your budget, the value of your car, and your driving habits. If you drive frequently, especially in high-traffic areas or hazardous locations, collision coverage can provide valuable protection. It's also important to assess your risk tolerance and financial situation. If you cannot afford to pay for repairs or replacements out of pocket, purchasing collision or comprehensive coverage, or both, is highly recommended.

The cost of collision and comprehensive coverage can vary depending on factors such as your insurer, location, and vehicle value. Generally, comprehensive coverage costs less than collision coverage. You can influence the cost to some extent by choosing different deductibles for each coverage. The deductible is the amount you pay out of pocket before your insurance starts paying for damages. By selecting a higher deductible, you can lower your premiums, and vice versa. However, having the same deductible for both collision and comprehensive coverage can make it easier to predict your out-of-pocket expenses in the event of any physical damage to your vehicle.

When filing a claim for paint delamination, it's important to act quickly. Contact your insurance company as soon as possible and report the damage. Before filing, review your policy to understand what is covered and under what circumstances. Your insurance will typically only pay for necessary repairs, so they may not cover repainting your entire car if only a single panel is affected. Additionally, consider if filing a claim is worth it financially. If the damage is minor, you may not meet your deductible, making it more cost-effective to pay for repairs yourself.

Transforming Mint Green to Gray Green: A Guide to Shifting Shades

You may want to see also

Explore related products

![]()

Vandalism and natural disasters

If your car has been vandalised, you may be able to file a claim with your insurance provider or pay for the repairs yourself. The latter option may be preferable if the cost of repairs is lower than your comprehensive deductible, as filing a claim could increase your premium rates.

Comprehensive coverage will usually cover vandalism, including keyed cars, slashed tires, broken windows, and any type of defacing of the vehicle. Theft often coincides with car vandalism and is also covered by comprehensive coverage. If you have comprehensive coverage, your insurance company will likely cover the cost of repairing paint damage caused by vandalism.

If your vehicle has received paint damage due to an act of vandalism, it is important to have your vehicle inspected by a professional. If the incident caused damage beyond surface paint damage, it is almost always in your best interest to file a claim with your auto insurance provider.

Home insurance typically covers damage caused by unforeseen events such as fires, vandalism, or natural disasters like hail or tornado damage. However, when it comes to painting projects, coverage may vary depending on your policy and the specific circumstances surrounding the damage. It's important to review your policy carefully to determine what is covered and what exclusions may apply.

Your homeowners insurance may cover damage to your home and belongings due to a covered peril, including damage from fire, wind, hail, and lightning. Damage from an earthquake or flooding is typically excluded from homeowners policies, and separate coverage must be purchased.

Dispose of Paint the Right Way in Columbia, SC

You may want to see also

Explore related products

![]()

Understanding your insurance policy

Types of Coverage

Depending on the type of insurance, paint damage may be covered under collision or comprehensive coverage. Collision coverage typically applies when there is damage to your car due to a collision with another vehicle or a stationary object. Comprehensive coverage, on the other hand, covers non-collision incidents, such as vandalism, theft, fire, falling objects, or weather-related damage. Some car insurance policies may also include uninsured motorist property damage (UMPD) coverage, which can provide protection if the other driver is at fault and uninsured.

Exclusions and Limitations

It is important to pay close attention to any exclusions or limitations outlined in your policy. For example, damage due to negligence or failure to maintain the painted area properly may not be covered. Understanding these exclusions will help you assess whether your claim is likely to be accepted or denied.

Deductibles

Before your insurance starts paying for paint damage expenses, you may need to pay a deductible, which is your share of the cost for a claim. The amount of the deductible will depend on your specific policy. In some cases, if the damage is minor, it may not exceed your deductible, and filing a claim may not be worth it.

Home Improvement Projects

If the paint damage is related to a home improvement project, carefully review your policy for any provisions or limitations related to these projects. Some policies may have specific coverage or exclusions for paint damage occurring during home improvements.

Documentation

Thoroughly document the paint damage with clear photographs or videos that show the full extent of the damage, including wide shots and close-ups. If the damage is to a structure, include reference points for scale. Additionally, gather and organize any relevant documentation, such as original receipts, contracts, appraisals, or invoices related to the painting project. This documentation will support your claim and help streamline the process.

Policy Terms and Conditions

Carefully review the fine print of your insurance policy to understand the specific terms and conditions outlined by your insurance provider. Pay close attention to any restrictions or limitations on paint damage coverage, as these can vary between policies and providers. Understanding these nuances will help you navigate the claims process and ensure you have a comprehensive understanding of your coverage.

Expanding Your Color Horizons in Paint Tool SAI

You may want to see also

Explore related products

![]()

Documenting the damage

Understanding Your Insurance Policy:

Before you begin documenting the damage, it is essential to review your insurance policy thoroughly. Understand your coverage limits, deductibles, and any exclusions or limitations that may apply. Pay close attention to provisions related to home improvement projects or specific circumstances mentioned in your policy. This step will help you navigate the claims process more effectively and increase the likelihood of a positive outcome.

Taking Photographs or Videos:

Use your camera or smartphone to capture detailed photographs or videos of the damaged areas. Ensure you take shots from various angles, including wide shots that showcase the full extent of the paint delamination and close-ups that highlight specific issues. If the damage is on a wall or structure, use reference points like a ruler to provide scale in your images. If you're claiming for artwork, capture the size of the piece, the details of the damaged areas, and its condition before the damage, if possible.

Gathering Supporting Documentation:

In addition to visual evidence, gather any original receipts, contracts, or appraisals related to the painted item or the paint job. These documents can provide proof of the item's value and the terms of service, especially if you're dealing with a botched paint job. Keep all receipts or invoices related to the painting project, including costs for materials and labour. This documentation will help streamline your claim and provide a record of repair expenses.

Writing a Detailed Account:

Prepare a written account of what happened, describing the incident that led to the paint delamination. Be as detailed and precise as possible in your written description. Include all relevant information and attach your photographic or video evidence. Transparency is key to a smooth claim process.

Communicating with Your Insurance Provider:

After you've documented the damage, contact your insurance provider as soon as possible to report the issue. Have your policy number ready, and be prepared to provide all the details surrounding the incident, along with your documentation and supporting evidence. Your insurance provider will guide you through the claim process and provide you with the necessary forms and instructions.

Quickly Cure Your Finger Paints 1-Step Gel Polish

You may want to see also

Explore related products

![]()

Reviewing exclusions and limitations

When reviewing exclusions and limitations in your insurance policy, it is important to pay attention to the fine print and understand the nuances of your coverage. Exclusions and limitations refer to specific conditions or circumstances under which your insurance company will not provide coverage for paint damage. These can vary depending on your insurance provider and the type of policy you have. Here are some key considerations when reviewing exclusions and limitations:

Type of Coverage

Determine whether you have collision or comprehensive coverage. Collision coverage pays for damage to your car if it collides with another vehicle or object, while comprehensive coverage covers damages not related to a collision, such as vandalism or natural disasters. Paint damage caused by flying debris or road conditions may not be covered under comprehensive insurance.

Negligence or Improper Maintenance

In some cases, if the paint damage occurs due to negligence or failure to properly maintain the painted area, your claim may be denied. This includes situations where the damage is a result of normal wear and tear or a lack of proper care.

Home Improvement Projects

If the paint damage is related to a home improvement project, carefully review your policy for any provisions or limitations specific to these projects. Some insurance policies may include coverage for paint damage during home renovations, while others may exclude it.

Cause of Damage

Understand the cause of the paint damage and whether it is covered under your policy. For example, damage caused by unforeseen events such as fires, water leaks, or natural disasters is typically covered, while damage due to sunlight, salt, or regular use may not be.

Coverage Limits and Deductibles

Before filing a claim, understand your coverage limits and deductibles. Some policies may have maximum payout amounts for paint damage claims, and you may need to pay a deductible before your insurance company covers the remaining costs. Weigh the cost of repairs against your deductible to determine if filing a claim is financially worthwhile.

Specific Policy Exclusions

Review your policy for any specific exclusions mentioned. For example, certain policies may exclude impact damage or paint delamination without an external cause. Understanding these exclusions will help you assess whether your particular case of paint delamination is covered.

It is important to carefully review your insurance policy and understand the exclusions and limitations to ensure a smooth claims process and increase the likelihood of a positive outcome. Don't hesitate to contact your insurance provider or agent for clarification if needed.

Transforming PNGs to ICOs with Paint 3D: A Guide

You may want to see also

Frequently asked questions

Yes, you can file an insurance claim for paint delamination, but it depends on the cause of the damage and your insurance policy. Delamination due to no outside cause is a warrantable condition, while damage from flying debris is not.

First, document the damage with clear photographs or videos, capturing the full extent of the damage. Then, review your insurance policy to understand what is covered and what exclusions may apply. Finally, contact your insurance provider and provide them with all the details and documentation of the damage.

Paint damage caused by unforeseen events such as fires, water leaks, vandalism, or natural disasters like hail or tornadoes is typically covered by insurance. Damage caused by collisions may also be covered, depending on your insurance policy.

Normal wear and tear, neglect, or failure to maintain the painted area properly are typically not covered by insurance. It's important to review your policy carefully to understand any exclusions or limitations that may apply.