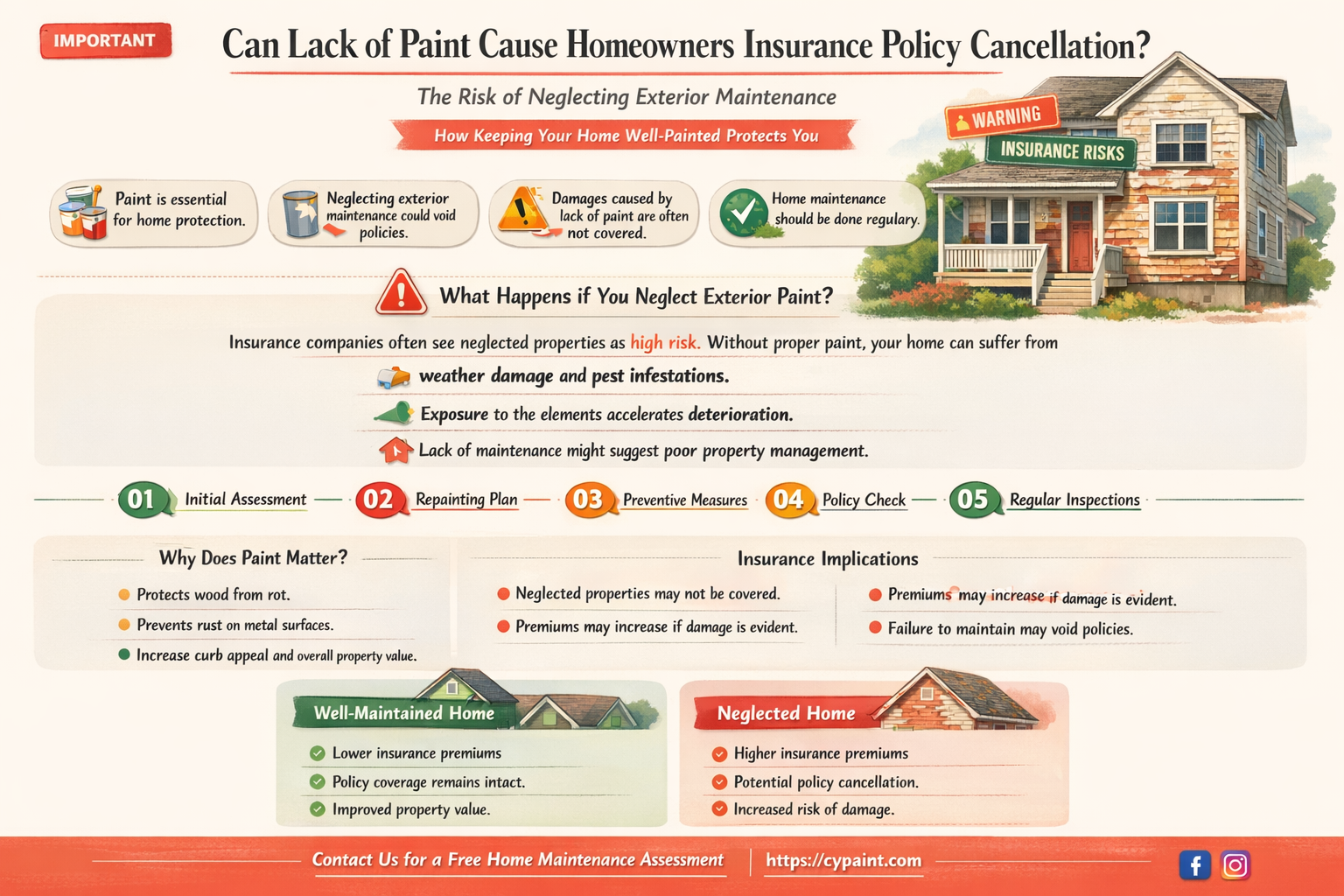

Homeowners insurance policies are designed to protect homeowners from financial losses due to damage or liability, but they often come with specific requirements and conditions that policyholders must meet to maintain coverage. One common question among homeowners is whether their insurance company can cancel their policy if their house is not painted or maintained to certain standards. While insurance providers typically focus on risks like structural integrity, safety hazards, or code violations, some policies may include clauses related to property maintenance. Failure to upkeep the property, including neglecting exterior paint, could potentially lead to policy cancellation if it significantly increases the risk of damage or diminishes the property’s value. However, the specifics vary widely by insurer and policy, making it essential for homeowners to review their contract and understand their obligations to avoid unexpected cancellations.

Explore related products

What You'll Learn

![]()

Reasons for policy cancellation

Homeowners insurance policies are not typically canceled solely because a house hasn't been painted. However, neglecting exterior maintenance, including painting, can lead to issues that insurers consider grounds for cancellation. Understanding these underlying reasons is crucial for policyholders to avoid unexpected terminations.

Insurance companies assess risk when determining policy terms. A home's exterior condition is a visible indicator of overall maintenance. Peeling paint, for instance, can signal potential problems like wood rot, moisture damage, or pest infestations. These issues increase the likelihood of costly claims, prompting insurers to reevaluate the risk associated with the property.

While painting itself isn't a direct policy requirement, it often falls under broader maintenance expectations outlined in insurance contracts. These clauses typically mandate that homeowners maintain their properties in a manner that prevents deterioration and minimizes risks. Failure to address issues like cracked siding, missing shingles, or, indeed, peeling paint, could be interpreted as a breach of these maintenance obligations, potentially leading to policy cancellation.

Some insurers conduct periodic inspections to assess a property's condition. If an inspection reveals significant neglect, such as extensive paint deterioration, the insurer may issue a notice requiring the homeowner to rectify the issues within a specified timeframe. Failure to comply could result in policy cancellation. It's essential for homeowners to review their policies carefully to understand the inspection process and any maintenance requirements.

To avoid cancellation risks, homeowners should prioritize regular exterior maintenance. This includes not only painting but also addressing issues like gutter cleaning, roof repairs, and landscaping to prevent water damage. Proactive maintenance not only preserves the home's value but also demonstrates to insurers that the property is well-cared for, reducing the likelihood of policy cancellation. Additionally, documenting maintenance efforts can provide evidence of compliance with policy requirements in case of disputes.

Mastering Lake and Tree Painting: Techniques for Stunning Landscapes

You may want to see also

Explore related products

![]()

Maintenance requirements in policies

Homeowners insurance policies often include maintenance requirements designed to mitigate risks and protect both the homeowner and the insurer. These clauses typically mandate that policyholders maintain their property in a condition that minimizes potential hazards, such as structural damage, mold, or fire risks. While painting a house might seem cosmetic, it can fall under these requirements if it serves a protective function, like preventing wood rot or rust on exterior surfaces. Failure to comply with these maintenance standards can lead to policy cancellation, as insurers may view neglect as an increased liability.

Consider the example of a wooden siding home. If the paint peels off, leaving the wood exposed, it becomes susceptible to moisture damage, termite infestation, or decay. Insurers may interpret this as a failure to uphold property maintenance, potentially triggering a policy review or cancellation. Policies often include specific language about "reasonable maintenance" or "preventative care," which can encompass tasks like painting, roof repairs, or clearing gutters. Homeowners should carefully review their policy documents to understand what constitutes acceptable upkeep.

From a practical standpoint, homeowners can proactively address maintenance requirements by creating a routine inspection schedule. Inspect the exterior of your home at least twice a year, focusing on areas prone to wear, such as siding, trim, and foundations. If paint is chipping or fading, repaint within a reasonable timeframe—typically every 5–10 years, depending on climate and material. Document all maintenance activities, including dates and descriptions, as evidence of compliance if questioned by your insurer.

While painting may not always be explicitly listed as a requirement, it often falls under broader maintenance expectations. Insurers prioritize risk reduction, and unpainted surfaces can signal neglect that may lead to larger, costlier issues. For instance, a neglected roof might develop leaks, or unpainted metal fixtures could rust, both of which increase the likelihood of claims. By staying ahead of these tasks, homeowners not only protect their investment but also ensure their insurance coverage remains intact.

Ultimately, maintenance requirements in policies are not arbitrary but rooted in risk management. Homeowners who treat these clauses as suggestions rather than obligations risk policy cancellation or denial of claims. To avoid this, adopt a preventative mindset: view painting and other upkeep tasks as investments in your home’s longevity and your insurance coverage. Regular maintenance not only preserves your property’s value but also demonstrates to insurers that you are a responsible policyholder, reducing the likelihood of disputes or cancellations.

Mastering Vibrant Art: Techniques for Painting with Dr. Martin Inks

You may want to see also

Explore related products

![]()

Homeowner responsibilities explained

Homeowners insurance policies often include maintenance requirements to mitigate risks, and neglecting these can lead to policy cancellation. For instance, failing to address issues like peeling paint or structural damage may violate your policy’s terms, as insurers view such neglect as increased liability. While simply not painting your house isn’t typically a standalone reason for cancellation, it can signal broader maintenance issues that insurers scrutinize. This highlights the critical link between homeowner responsibilities and policy compliance.

Analyzing policy language reveals that insurers prioritize risk management. Most policies require homeowners to maintain their property in a "reasonable state of repair." Peeling paint, for example, can indicate underlying problems like water damage or rot, which elevate the risk of claims. Insurers may inspect properties if they suspect neglect, and repeated failures to address maintenance issues can result in non-renewal or cancellation. Thus, painting isn’t just cosmetic—it’s a preventive measure tied to structural integrity.

To avoid policy complications, homeowners should follow a proactive maintenance schedule. Inspect your property seasonally, focusing on areas prone to wear, such as siding, roofs, and foundations. Address minor issues like cracked paint or loose shingles promptly, as these can escalate into costly repairs. Keep detailed records of maintenance activities, including dates and descriptions, to demonstrate compliance if questioned by your insurer. Think of it as preventive care for your home, similar to regular health check-ups.

Comparatively, renters face fewer maintenance burdens, but homeowners bear the full responsibility for their property’s condition. This includes both visible and hidden issues. For example, while a faded exterior might seem minor, it could mask deeper problems like wood rot or pest infestations. By staying ahead of maintenance, homeowners not only protect their investment but also ensure their insurance remains valid. Neglecting these duties can leave you financially vulnerable in the event of a claim denial.

In conclusion, homeowner responsibilities extend beyond aesthetics—they’re about risk management and policy adherence. Painting your home isn’t just about curb appeal; it’s a tangible way to demonstrate care for your property. By understanding and fulfilling these obligations, you safeguard both your home and your insurance coverage. Treat maintenance as a non-negotiable task, and you’ll avoid the pitfalls of policy cancellation.

Unveiling the Science: How Paint Adheres to Shiny Cardboard Surfaces

You may want to see also

Explore related products

![]()

Avoiding insurance cancellation tips

Homeowners insurance policies can be canceled for various reasons, and while a lack of paint maintenance might not be the most common cause, it can still pose a risk. Insurance companies assess properties for hazards, and a neglected exterior could signal potential issues. For instance, peeling paint may indicate underlying problems like water damage or rot, which could lead to costly claims. Understanding this, homeowners can take proactive steps to ensure their policy remains active.

Inspect and Maintain Regularly: A preventative approach is key. Schedule bi-annual inspections of your home's exterior, focusing on areas prone to wear and tear. Look for signs of paint deterioration, such as cracking, bubbling, or fading. Address these issues promptly by repainting or hiring professionals for more extensive repairs. Regular maintenance not only preserves your home's aesthetic but also demonstrates to insurers that you're mitigating risks.

Understand Policy Requirements: Delve into the specifics of your insurance policy. Some policies may include clauses related to property maintenance, outlining the insurer's expectations. These clauses could provide insights into what might trigger a cancellation. For example, a policy might require homeowners to maintain the property in a 'reasonable state of repair,' leaving room for interpretation. Knowing these details empowers you to take targeted actions to stay compliant.

Document Your Efforts: Keep a detailed record of all maintenance activities, including dates, descriptions, and, if applicable, invoices from contractors. This documentation serves as evidence of your proactive approach to property care. In the event of a policy review or cancellation threat, you can present this information to demonstrate your commitment to maintaining a well-kept home. It's a simple yet effective way to advocate for yourself and potentially negotiate with insurers.

Consider the Bigger Picture: While paint maintenance is essential, it's part of a broader home care strategy. Insurers assess overall risk, so ensure other aspects of your property are also well-maintained. This includes keeping the roof in good condition, addressing plumbing issues promptly, and maintaining a safe electrical system. By taking a holistic approach to home maintenance, you not only reduce the chances of insurance cancellation but also create a safer and more valuable living environment.

Stay Informed and Communicate: Insurance policies and their requirements can evolve, so stay updated on any changes. Regularly review your policy documents and communicate with your insurance provider. If you're unsure about specific maintenance expectations, ask for clarification. Open communication can prevent misunderstandings and allow you to address any concerns before they become issues. Being proactive in this manner is a powerful tool in avoiding unexpected policy cancellations.

Setting Up a Painter: Palette Essentials

You may want to see also

Explore related products

![]()

Disputing cancellation decisions

Homeowners insurance policies can be canceled for various reasons, and while lack of maintenance like unpainted exteriors is rarely a direct cause, it can lead to broader issues that trigger cancellation. For instance, untreated surfaces may deteriorate, increasing the risk of damage, which insurers might view as negligence. If your policy is canceled under such circumstances, disputing the decision requires a strategic approach.

Step 1: Review Your Policy and Cancellation Notice

Begin by scrutinizing your insurance policy for clauses related to maintenance or conditions that justify cancellation. Pay attention to terms like "hazardous conditions" or "failure to mitigate risk." The cancellation notice should specify the reason; if it’s vague or unrelated to painting, request a detailed explanation in writing. Highlight any discrepancies between the policy terms and the insurer’s justification to build your case.

Step 2: Document and Address the Insurer’s Concerns

If the cancellation stems from perceived neglect, gather evidence to counter the claim. Provide photos, receipts for recent maintenance, or contractor estimates for pending work. For example, if the insurer cites peeling paint as a risk, show proof of scheduled repairs or ongoing efforts to address the issue. Insurers often prioritize risk mitigation, so demonstrating proactive steps can strengthen your dispute.

Step 3: Leverage State Regulations and Ombudsman Services

Insurance regulations vary by state, and many prohibit cancellations without valid cause or proper notice. Research your state’s laws to ensure the insurer complied with legal requirements. If the cancellation seems unjustified, file a complaint with your state’s insurance department or ombudsman. These entities can mediate disputes and compel insurers to reverse decisions if they violate regulations.

Caution: Avoid Escalation Without Evidence

While disputing a cancellation, avoid confrontational tactics without solid evidence. Insurers may view aggressive disputes as adversarial, potentially complicating resolution. Instead, maintain a professional tone and focus on factual arguments. If the dispute escalates, consult an attorney specializing in insurance law to navigate legal complexities.

Even if you successfully dispute a cancellation, address the underlying concerns to avoid recurrence. Regular maintenance, such as repainting every 5–7 years, not only preserves your home but also aligns with insurers’ expectations. Proactivity not only safeguards your policy but also reduces long-term risks, ensuring your home remains insurable.

Creative Milk Jug Painting Guide for Divers: Easy DIY Tips

You may want to see also

Frequently asked questions

Yes, homeowners insurance companies can cancel or non-renew your policy if your home is not properly maintained, including issues like peeling paint, as it may indicate neglect that could lead to larger structural problems or increased risk of damage.

Regularly inspect and maintain your home’s exterior, including repainting as needed to prevent deterioration. Document maintenance efforts and communicate with your insurer to demonstrate proactive care of your property.

Immediate cancellation is less common, but repeated failure to address maintenance issues like unpainted surfaces can lead to non-renewal or cancellation at the end of the policy term, depending on the insurer’s guidelines and state regulations.